You have arrived at this article via a link found in the September/October No Greater Joy Magazine or have been provided the link from one of our readers. To download this article as a PDF, click here.

It is always good to know the background of the person writing the article. Since many of you do not know my background, here it is:

Mel Cohen

Certified Financial PlannerTM

Registered Tax Return Preparer

CURRENT AND FORMER MEMBERSHIPS, AFFILIATIONS AND ASSOCIATIONS

A Biographical Record appeared in the Silver Anniversary 28th Edition of Marquis Who’s Who in Finance and Industry as well as the Thirty-first 2000/2001 Millennium Edition, inclusion in which is limited to those individuals who have demonstrated outstanding achievement in their own fields of endeavor and who have, thereby contributed significantly to the betterment of contemporary society.

I have been the CFO or compliance manager for ministries ranging in size from $3 million to $28 million in annual revenue prior to joining No Greater Joy Ministries.

This article is general information only. Mel Cohen is not engaged in rendering investment or professional advice to the reader. If investment or professional assistance is required, the services of a competent professional advisor should be sought.

From the predictions of Jonathan Cahn, a Messianic Rabbi and best-selling author, to Ron Paul, a former Congressman, to many prominent financial advisors, the latter part of the third quarter and the fourth quarter of this year may be extremely volatile in financial markets throughout the world. Many of the financial advisors are predicting 50%-60% drops in the stock market! Many of these same advisors do so to encourage you to sign up for their various newsletter subscriptions or publications, as good news rarely sells. Bad news sells well!

When President Obama took office on January 20, 2009, the National Debt stood at $10.6 trillion. It is now an alarming $18.1 trillion, a $7.5 trillion increase (https://www.usgovernmentdebt.us/state_debt). More alarming is about $3.3 billion a day is being added to that number. This equates to about $55,000 of debt per person as this article goes to press. This is a situation that cannot go on forever. Someday there will be a price to pay for this foolishness!

A little over a third, or $6.2 trillion, is owed to foreign investors, another $2.6 trillion to domestic investors, $2.5 trillion to the Federal Reserve, plus $5.1 trillion to federal accounts with the balance being owed to state and local governments and miscellaneous categories. The second largest debt is owed to the various federal accounts which borrow money from one fund for use in another fund. The Social Security Trust Fund often lends to other branches of the government. If you want to see the debt in real time, visit https://www.usdebtclock.org/. The above numbers will vary depending on the source and when you look them up. The interest alone on this debt is about $2.3 billion dollars a year.

The government takes money from one group of individuals (mainly through taxes) and gives them to another group of individuals they feel needs them. I am fully supportive of temporary programs to help those in need, but not to the degree the government doles out money to unproductive individuals, and often over multiple generations. In 2014, over half of the country paid no income tax. Many not only paid no taxes, but they received tax refunds on top of that. This cannot go on forever. About 25% of workers paid almost 90% of all federal income taxes.

Former Social Security/Medicare Trustee Tom Saving (an economist at Texas A&M University) and his colleague, Andy Rettenmaier, have analyzed the most recent Trustees’ report. Looking indefinitely into the future, the unfunded liability in both programs is $72 trillion! And that assumes the Medicare cuts legislated by ObamaCare hold fast. If they don't, the unfunded debt will exceed $100 trillion—about six times the size of the entire economy.

Add another trillion dollars to state debt, and more to local government debt. No wonder as of March 31, 2015, total household indebtedness was $11.85 trillion. The Federal, State and Local governments have set a bad example for the average family (https://www.newyorkfed.org/microeconomics/hhdc.html).

The debt you’ve probably never heard of has reached into the multitrillion-dollar range. Warren Buffett, Berkshire Hathaway’s chairman, has warned that state funding for pensions is “woefully inadequate.” This shortfall in defined-benefit pension plans will have to be made up by taxpayers, bondholders and state pensioners.

In 2012 a book by Jonathan Cahn entitled The Harbinger was released. It is estimated that it sold a million copies in the first year and is still going strong. It is based on Isaiah 9:10 judgments of Israel and their relevance to the United States. One of the chapters in the book is entitled The Mystery of the Shemitah (this is not an endorsement for either book) which led to a second book by the same name.

Add these books to all of the blood moon books predicting financial chaos, along with Congressman Ron Paul’s infomercial on a financial collapse to get you to purchase a book and a newsletter subscription on how you can survive this. These books, along with other doomsday predictions by those selling subscription-based newsletters, have created uncertainty in the lives of many families.

Many of you will be reading this after the fact, so we will all learn together how accurate these trouble signs are which could affect the financial future and well-being of millions.

Dates

Last day of the current Shemitah: September 13, 2015.

Per Safe Money Report: September 16, 2015 a secret meeting is to take place in Washington D.C., “an event will take place that will change everything in your life.” The author is calling it “Bloody Wednesday.”

The Federal Open Market Committee will hold its sixth meeting this year on September 16-17. The prior meeting (https://www.federalreserve.gov/newsevents/press/monetary/20150729a.htm) kept the federal funds rates the same at 0 to ¼ percent. Many economists fear that the fed will raise the interest rate.

If this happens, the most direct effect is banking! A rate increase makes it more expensive for banks to borrow money from the Fed. Bank loans, credit card fees and any loans tied to adjustable rates will be affected by a rate increase. When a family has to spend more on interest payments, they have less money to spend on everything else which can have an adverse effect on the overall economy. Read more: https://www.investopedia.com/articles/06/interestaffectsmarket.asp#ixzz3ic5Gu8nM

The fourth and final blood moon: September 29, 2015. A blood moon is another name for a full lunar eclipse. When the shadow of the earth completely blocks the sun’s direct rays, the moon takes on a reddish or red-orange color. Three of the four blood moons have already occurred: April 15, 2014; October 8, 2014; and April 4, 2015. Between the first two blood moons there was a total solar eclipse which fell on March 20, 2015 which is the first day of the Biblical New Year of the Jewish calendar.

When there are four consecutive full lunar eclipses with no other intervening eclipses, it is called a tetrad (Latin for 4). All four full lunar eclipses fall on Jewish feast days (Passover and the Feast of Tabernacles) in the spring and fall of 2014 and 2015. This has happened nine times over the last 2,000 years. This phenomenon has ignited prophecy teachers putting forth doomsday predictions based on Joel: 2:30-31 And I will shew wonders in the heavens and in the earth, blood, and fire, and pillars of smoke. The sun shall be turned into darkness, and the moon into blood, before the great and terrible day of the Lord to come.

Scheduled International Monetary Fund (IMF) Meeting: October 20, 2015. Some financial experts predict that the Chinese Yuan will be added to the seven other currencies that are part of the IMF. This would be the first change in about 35 years. About 60% of the world’s reserve currencies are held in the US dollar. Any change in the reserve currency would be felt around the world and cause an adverse effect on the dollar. Reserve currencies are used in global trade (business) while governments use them to diversify their investments and pay down debt.

Why the Concern? About $1.5 trillion of our foreign debt is owned by China. Over 10,000 businesses treat the Yuan as a reserve currency. In the last four years this has gone up over one thousand per cent. There are twelve major banking centers that are Yuan clearing houses. China is hoarding gold and hopes to have the Yuan as the only currency fully backed by gold. Any one or two of these facts would not cause concern; couple all of them together and there is grave concern about the financial future and power of the US especially as compared to China which is second to the US in many economic categories.

The dollar is widely accepted and used throughout the world. When countries trade or purchase commodities from other countries their currencies must first be converted to dollars. The trades are settled in dollars. The dollar is the strongest world currency as of this writing. This is why our imports are so much cheaper and our inflation has been kept under control. It takes fewer dollars to purchase foreign goods since the dollar is so strong. If you are exporting, the strength of the dollar will hurt your business as more of the trading country’s currency must be used to buy in dollars.

A popular political saying is, “Are you better off today than you were four years ago?” Go back six months, one year, two years, or even five years and see what has improved or is better today than the time period you select.

The worldwide threat of terrorism from ISIS/ISIL, Al Qaeda, Boko Haram, etc.—is it better or worse? The brutality and savagery these groups do on a daily basis is unprecedented in modern times especially against Christians. From setting people on fire, to beheadings, to having their prisoners kneel on explosives are crimes against humanity these terrorists do on a daily basis. Add to this the slave trafficking they are responsible for creates a crisis much of the world seems to be overlooking.

Consider Iran’s nuclear ambitions. History has clearly shown they cannot be trusted. They are funding conflicts throughout the Middle East and may soon destabilize the entire region. Is it better or worse? The recently signed Nuclear Deal has yet to be approved by Congress. Whether approved or not, it will have a far reaching affect throughout the world.

Genesis 12:1-3: Now the Lord had said unto Abram, Get thee out of thy country, and from thy kindred, and from thy father's house, unto a land that I will shew thee: 2 And I will make of thee a great nation, and I will bless thee, and make thy name great; and thou shalt be a blessing: 3 And I will bless them that bless thee, and curse him that curseth thee: and in thee shall all families of the earth be blessed. Whether it is the Iran Nuclear Deal, the lack of trust and support from President Obama or many the turning against the Nation of Israel by many US-based Christian organizations spouting “Replacement Theology,” the lack of support for Israel may cause the Lord to withhold the many blessing He has poured on the US.

North Korea has been exporting their nuclear and missile technology to countries that would not be considered friendly to the US. Is it better or worse?

The recent aggression Russia has shown in the Ukraine and the threats of more aggression by building 40 new nuclear ballistic missiles. Is it better or worse?

China’s flexing of their military muscles and island building (over 2,000 acres) to create new sovereign territory. What happened to freedom of navigation and freedom of the seas in international water? Is it better or worse?

The decline of morals in the US, sexual signs that were once against the law are no longer, the passage of same-sex marriage. The US joined twenty other countries in passing this. Is it better or worse?

Wealth gap between the rich and the poor—is it better or worse?

A 30-year-old suspect has been arrested after police found two women and three girls dead in a California home on July 19, 2015.

More threats from major terrorist organizations threatening to attack military installations similar to the attack that killed four marines and a US Navy Petty Officer on July 16, 2015.

Movie theater attack in Lafayette, LA by a man that killed two women before killing himself on July 23, 2015

Movie theater attack by a man with a hatchet and pepper spray on August. About three years earlier was the Aurora, CO shootings that killed 12 people.

Senseless killings: the latest in Houston on August 8, 2015 had eight members of one family killed. About a year earlier six members of one family were killed in Spring, TX, a suburb of Houston.

There has been a dramatic increase in homicides in many large and mid-sized cities throughout the US.

Violent crimes including murder committed by illegal aliens. On August 10, 2015, California Governor Jerry Brown signed a law that bans the word “alien” from the state’s labor laws.

Sanctuary Cities: There are over 200 cities that follows certain procedures that shelters illegal immigrants. Some by law (de jure) others by action (de facto) prevent criminal aliens from deportation by refusing to comply with ICE detainers and impede open communication and information exchanges between their employees or officers and federal immigration agents. The designation of “Sanctuary City” has no legal meaning.

The protests that have happened and are happening now throughout the US in cities like Ferguson, MO, Cincinnati, OH, Stonewall, MS, Baltimore, MD and many others which cause unrest, fear, loss of property and most importantly loss of life.

I no longer possess the credentials to provide investment advice so I am writing from a personal perspective not a professional one.

Years ago I was a follower of Larry Burkett (died July 4, 2003) who founded Christian Financial Concepts which later merged with Crown Financial Ministries in the year 2000 (https://www.crown.org/). He was one of the best financial counselors around at the time; his advice mainly coming from Scripture. I read his books, followed his budgeting ideas even took his course on being a counselor. His budgeting ideas were clearly presented and helped many get out of debt. The modern “Get out of Debt” mantra has been passed to Dave Ramsey (https://www.daveramsey.com/home/). GET OUT OF DEBT!

Proverbs 22:7 The rich ruleth over the poor, and the borrower is servant to the lender. Over the years as a CFP and financial counselor, I have seen debt destroy the harmony many families had before debt took over their lives and made all decisions revolve around finances. I looked at several national polls on “Why married couples get divorced.” Finances or money was in the top five of almost every poll. If money is a consistent topic of disagreement, divorce for many seems the only option.

Between job losses, illnesses, home catastrophes and other emergencies, everyone should have an emergency fund. This is the amount of cash that you readily have on hand in the event that you cannot generate income through your employer— or earnings if you are self-employed.

The amount of funds you may need depend on how much cash is spent on a monthly basis on mandatory spending (mortgage, taxes, gas, food, etc.) versus how much cash comes in on a monthly basis (social security, pensions, IRA, interest, dividends, etc.) even if you cannot work.

If you have children in the house, with only one worker you may need as much as nine months of cash— if you are older with no children in the house you should be able to get by with three months of emergency fund cash.

Unfortunately, world economies are greatly entwined. What happens throughout the world does affect us in our everyday living.

As the dollar rises, imports become less expensive, but exports become more expensive. What is good for the average consumer in the US is bad for the manufacturers whose profits depend on the amount of goods they produce for export. Also, the food and beverage companies like McDonald’s and Coca Cola that depend on sales outside the US, will suffer. Outside the US, McDonald’s sales are about 68%, while Coca Cola is about 75%.

Earlier this year, the global consulting firm McKinsey & Co. issued a report on the 20 most-indebted nations.

The numbers are shocking.

Just below those top 20 nations we have Canada at #21 with debt-to-GDP at 221%, Australia at #23 with 213%, and Germany at #24 with 188%. The most prudent Western nation is tiny Slovakia at #27 with 151% debt to GDP.

Overall, global debt now sits right at $200 trillion — nearly three times larger than the world’s entire economic output in a given year.

Many of our readers are young and raising a family and have not had the ability to develop an investment strategy. I strongly urge you to look at these links to help you in your ability to eventually accumulate an investment portfolio. Although some of the information is a bit dated, it is a good foundation for starting out. I had the privilege of speaking at the 2013 and 2014 NGJ Shindigs. 2013 was entitled Investing in Troubled Times and 2014 was Family Finances and Budgeting. The 2013 Shindig Seminar link is: https://ngj.me/wiseinvesting, the 2014 Shindig link is: https://ngj.me/2014-seminar and 2014 Shindig Video Link is: https://ngj.me/melvids.

For those that are invested in the stock market, I suggest you work with your broker or independent advisors to protect the gains you have accumulated since the market recovery. As an FYI, I am no longer a Registered Investment Advisor, so I would not be the one able to provide advice or consultation through this article or by phone. What I will write below is only my own opinion.

When the NASDAQ crashed in March of 2000, it took over 15 years to get to the point of where it was on the day of the crash. That is a long recovery. When the Dow and the S & P 500 tanked in 2007-2008 it only took a few years to recover to where it was, and we have had about 7 years of strong gains in the equities market.

Being older and wiser now, I reduced the amount of equities I own. For my age I should have less than 30% equities. About 4 months ago when I started to analyze my portfolio I discovered I was over 90%. I started a systematic method to reduce that, by selling off the few stocks I had that were in negative territory. Today my equity ratio to cash, cash equivalents, silver and gold bullion is less than 50%.

The stock market is also known as the equity market. It trades and issues shares of publicly held companies through exchanges or over-the-counter markets. The primary goal of the market is to provide companies with capital. When you invest in the market, you are acquiring ownership in a company. Over time small amounts of money can grow into large amounts of money if invested wisely. There is risk—what goes up often will come down! Stocks that pay dividends offer another way to grow your investment. Dividends can be taken as cash payments when issued or used to repurchase the same stock at the current market value. A dividend reinvestment program is also called a DRIP. There are many investing strategies.

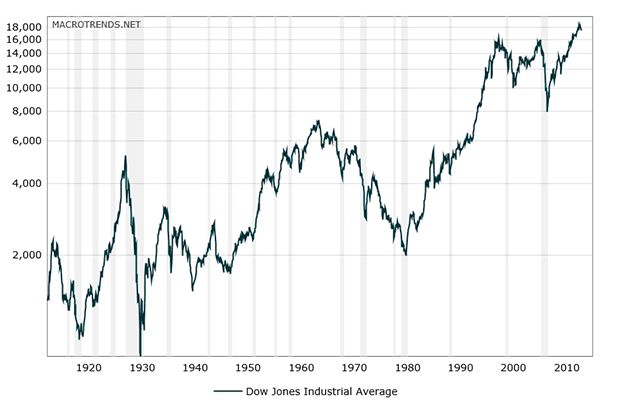

The Dow is the most widely quoted index. Usually the first report on various business networks quote the Dow-same with financial publications and investing newsletters. Ironically the Dow consists of only 30 stocks. They are the 30 largest companies in our economy. They are not all industrial companies as the name indicates. The Dow was founded in 1896 with only 12 industrial companies being listed. General Electric is the only company that was on the list in 1896 and is still on the list today.

In the current Dow, financial service firms represent about 25% of the index while Industrials are second. There are several other sectors consisting of consumer services, technology, health care, and oil and gas companies. The Dow is one of the most common measures of how the U.S. stock market is doing. In its early years, the performance was mostly affected by how the industrial stocks performed. Today corporate and economic reports along with worldwide events such as war, terrorism, large scale natural disasters, disease, and countries’ financial defaults all affect the Dow.

The Dow has only changed 51 times since 1896. The most recent change was Apple replacing AT & T in March of 2015. The 30 companies that make up the Dow are:

MMM 3M - AXP American Express - AAPL Apple - BA Boeing - CAT Caterpillar - CVX Chevron - CSCO Cisco - KO Coca-Cola - DIS Disney - DD E I du Pont de Nemours and Co - XOM Exxon Mobil - GE General Electric - GS Goldman Sachs HD Home Depot -IBM IBM - INTC Intel - JNJ Johnson & Johnson JPM JPMorgan Chase - MCD McDonald's - MRK Merck - MSFT Microsoft - NKE Nike - PFE Pfizer PG Procter & Gamble - TRV Travelers Companies Inc - UTX United Technologies - UNH UnitedHealth - VZ Verizon - V Visa - WMT Wal-Mart.

Dow Jones 100-Year Historical Chart

The two largest stock exchanges in the US are the New York Stock Exchange and the NASDAQ. For a more detailed definition, see https://www.investopedia.com/terms/s/stockmarket.asp#ixzz3iXnowhTL.

Bonds are debt instruments. The two main components are corporate debt which is issued by publicly held companies that want to borrow money for operating expenses or capital improvements, rather than issue stock which provides equity. Government issued securities are issued from the federal, state and local level to fund ongoing operations or long term capital improvements. The bond market is much larger than the stock market, and consists of the primary market which sells directly from the borrower to the lender, and secondary market which sells or resells previously issued securities. For a more detailed definition see https://www.investopedia.com/terms/b/bondmarket.asp#ixzz3iXuIpMna.

Set your Timeframe: Determine the time horizon for your investments as each time frame will have a different strategy. Short term is 1-3 years; mid-term 4-9 years; any time beyond that is considered long term. The closer you get to your timeframe, the less risk you can afford to take. Mid-term may be the trickiest as you want to invest for gain, but cannot take too much risk—balance is needed. A general rule in investing is when you have a longer time frame for your financial goals, more investment risk can be taken. See more at: https://www.finra.org/investors/set-time-frame-your-financial-goals#sthash.VTvQqb7K.dpuf

Invest in what you understand. If the investment vehicle cannot be clearly explained in 1-2 sentences, it may not be good for you. There are a few investment advisors that are willing to risk your money for sales commissions.

Use a strategy of investing in index funds. Index funds are simply mutual funds that are based on an index and mirror its performance. An example is the S & P 500. For all 20 year periods since 1926 which was 3 years before the Great Depression of 1929, the S & P 500 has returned an average of 7.25%.

Start Early. Take advantage of compounding over a long period of time, and dividend reinvestment (DRIP) strategies.

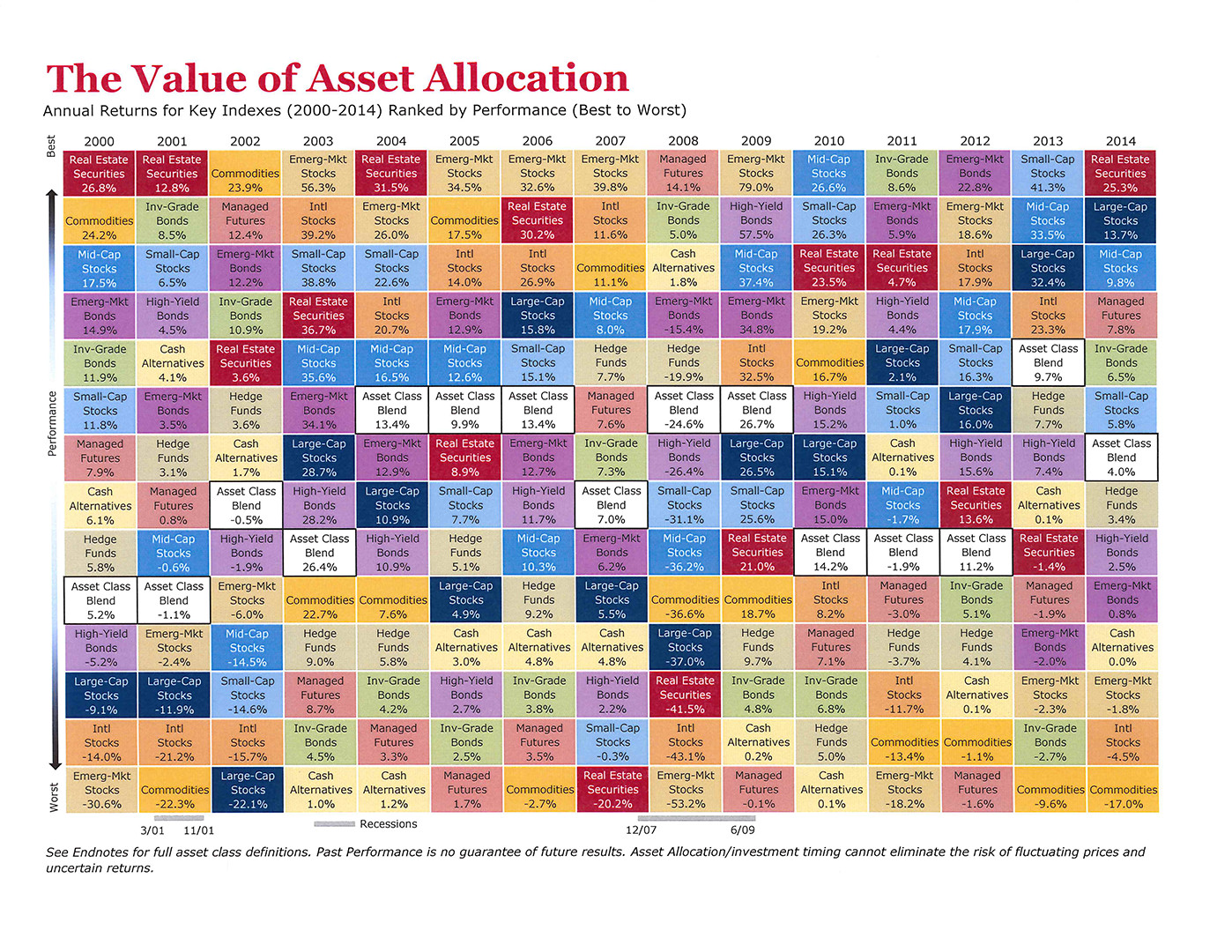

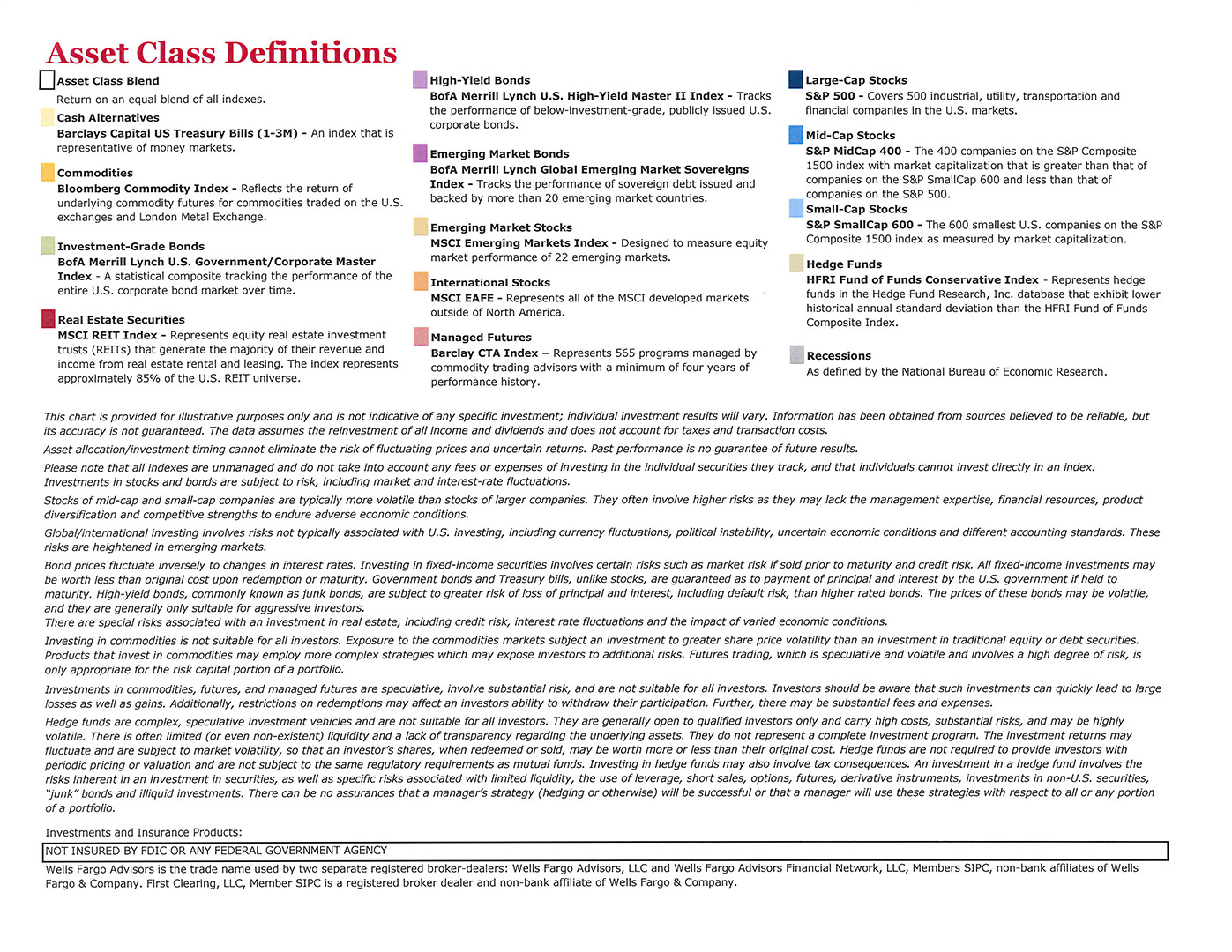

Diversify across several asset classes and also within an asset class. See chart at the end of this document, “The Value of Asset Allocation.”

Retirement Plans: if your company has a 401(k) match or any other type of match up to a certain percentage, take full advantage of that. EXAMPLE: If your company matches the first 3% of your investment and your 3% equals $2,000, your company would then put in $2,000 so your total investment is now worth $4,000. You have doubled your money or a 100% instant return on your investment.

How millionaires are made: Taking the average rate of return of the S & P 500 of 7.25% and investing $5,500 into a ROTH IRA, starting at age 22 and stopping at age 66, the amount of your investment would be worth $1,688,352. Under current law a ROTH held for this period of time would allow the participant to withdraw this money on a tax-free basis—it would be all yours. There is no mandatory withdrawal on a ROTH compared to a traditional IRA which requires mandatory withdrawals starting at age 70 ½. Mandatory withdrawals are taxable.

A good website for mortgage rates, CD rates, money market rates and financial calculations is www.bankrate.com.

Emergency Fund: Keep that separate from your investible funds. In a true emergency you may need cash or a cash equivalent within the same day or next day. You do not want to have to sell something that may not be liquid, such as real estate, due to the emergency time frame. Read more: https://www.investopedia.com/university/indexes/index8.asp#ixzz3ijHuVwZk

If all of the warnings signs on the economy do not play out—much like Y2K—and the stock market were to rise up over the next 8 weeks, I may give up a few percentage points of gain, which I am willing to do for safety. If the market corrects or enters into a bear market (20% or more drops) I have saved a loss of my net worth. The older one is, the more concerned they have to be with safety of principle versus chasing gain, as we do not have time for a full market recovery.

It took over 15 years for NASDAQ to break its record of where it was in March of 2000 (5,048.62). On April 23, 2015 it closed at 5,056.06, the next day it broke the record of April 23rd. In 2002 it had a record low of 1,114.11 which represents a gain of over 3,900 points from the low to the new high. At today’s close August 13, 2015 the number was 5,033.56.

When stocks drop they pose a strong buying opportunity. If big names like Coca Cola, Walmart, Microsoft, McDonald’s or any other household names, drop 30%-40% because of world events, it is a time to buy—I have set aside enough cash where I could buy these stocks at great discounts compared to their true value. Buy low, sell high is a strategy we all dream about, but few follow because of emotions. Take emotions out of investing and you will have a stronger portfolio value—know your purpose for investing. I have learned to take the emotion out of buying and selling stocks or any other investments.

A good way to protect your portfolio is to use trailing stops. Set a percentage on a per stock basis, such as 12% to 20%. When that stock drops by that percentage, it will sell automatically.

Over the last year or so gold and silver have had a strong drop in pricing. I took the money I had from the sale of stock and invested some of it in US American Eagle Silver Dollars .999% pure silver. It is the most recognized bullion coin in the world. I do not look at silver or gold as an investment, I look at it as insurance. I take possession and within a day or so of arrival they are put into a safe place out of my house. I do not trust these gold or silver providers that will “store silver” for a fee or issue a certificate for your silver which can be redeemed anytime. The “redeemed anytime” is what scares me, especially if there were a true economic crash.

In the event of a financial collapse of the dollar, and people will not take dollars for some reason, they will certainly take silver. I initially preferred silver over gold as a single silver coin is worth $20 or so. If we needed emergency milk or groceries, silver is easier to deal with than a one-ounce gold coin that is worth about $1,100. For years a good rule of thumb has been 5%-10% of your portfolio should be in silver or gold. I have increased mine to about 12%. I like the one-ounce US American Eagle coins better than the heavier-weight bars for potential ease-of-use and worldwide recognition.

When purchasing silver or gold, shop around for the best buy. When you purchase online you will usually receive a better price than if you were to call and talk to a representative to buy (no commissions). Reps will often pressure you into more expensive pieces that pay them a high commission, which in reality you are paying.

There are other ways to own gold: through the equities (stock) market. Electronically Traded Funds (ETF) often mirror the market. Over a period of six years, which ended in December 2012, the price of gold went up over 155%, while the gold stock fund GLD rose 160%. Since then, both have gone the other way.

Governments can print all of the money they desire to increase the money supply (which they have done), but they can’t print GOLD!

Definition: The gold-to-silver ratio is the amount of silver it takes to purchase one ounce of gold. Take the price of gold, divide it by the price of silver, and you have the gold-to-silver ratio. On August 12, 2015 at 11:33 a.m. CT that ratio was as follows: silver $15.59-Gold $1,124.25 or slightly over 72 times. This means it would take 72 plus ounces of silver to purchase one ounce of gold.

Many experts feel that when gold is over 50 times the price of silver it is a good buy sign for silver. If under 50 times gold may be the better value for growth. About 10 times in the last 15 months I have bought silver, but only bought gold twice.

As the dollar tends to strengthen gold will present itself as a stronger buy. The true value of silver or gold has not changed over the past year or so, but the strong dollar made it cheaper to purchase during late July, which was the cheapest prices for these metals any time in the past five years. Both metals in the last few days have been on the rise. The gold-to-silver ratio over the past 30 days has been 72.22 to 76.44. One year ago it was 65.23 to 77.08. Five years ago 32.00 to 72.08 while ten years ago it was 32.00 to 83.86. There were times over the past ten years that gold would be a better value compared to today, when silver seems the better buy.

Many financial advisors recommend this strategy (DCA) when there is a large amount of money to invest. The main reason is that if the market were to go down suddenly it would not affect the amount of money that is on the sidelines. Conversely if the market were to go up, you would lose the potential gain by not having those dollars invested. If you feel the market is headed up for gold and silver, than buying now would be the best strategy as your initial investment would increase as the price of gold or silver increases.

If you feel the market will continue to go lower; waiting for the market to bottom out may be a better strategy, but there is risk of a sudden reversal. I have used DCA over the past 15 or so months and will continue to do so as I believe the markets will go lower in gold and silver over the next month or so, but if they don’t and increase suddenly, my average cost and previous purchases were protected.

Record keeping on gold and silver started in 1687. Since then, the gold-to-silver ratio has been between 14 and 100. During most of the twentieth century the gold-to-silver ratio has averaged about 47-50, with wild fluctuations.

This article has primarily focused on finances and financial preparation. If trouble breaks out because of financial unrest, you would be wise to have prepared and secured your home. Make sure you have enough water, food, source of fuel, first aid supplies, emergency supplies, toiletries, clothing, bedding, and if on prescription medicine a 2-3 months’ supply.

Only the Lord knows if the next several months will bring about economic instabilities. But you can be informed and prepared to wisely steward the resources which He has entrusted to you.

“Go to now, ye that say, To day or to morrow we will go into such a city, and continue there a year, and buy and sell, and get gain: Whereas ye know not what shall be on the morrow. For what is your life? It is even a vapour, that appeareth for a little time, and then vanisheth away. For that ye ought to say, If the Lord will, we shall live, and do this, or that” (James 4:13-15).

Click a page thumbnail below to enlarge.

Download this entire article as a PDF.

This article is general information only. Mel Cohen is not engaged in rendering investment or professional advice to the reader. If investment or professional assistance is required, the services of a competent professional advisor should be sought.

Thank you No Greater Joy Ministries for allowing me the time to write this article.

Copyright © Mel Cohen, August 2015

You must be logged in to post a comment.

I have no greater joy than to hear that my children walk in truth. 3 John 4

© 1995–2024. No Greater Joy Ministries (NGJ) is a 501(c)(3) nonprofit ministry of Michael and Debi Pearl.

NGJ is a Member of the Independent Book Publishers Association.

My wife and I have debt AND health issues. We live on fixed incomes. We're aware of what the future holds and that a financial collapse is imminent.

Should we concentrate on our health or debt retirement? We can't do both simultaneously.

I would concentrate more on health issues than debt retirement. Still try to make the wisest most economical choices regarding caring for your health, but if I had to make a choice it would overwhelmingly be health. Since I do not know your financial situation this is personal advice not professional advice. -Mel